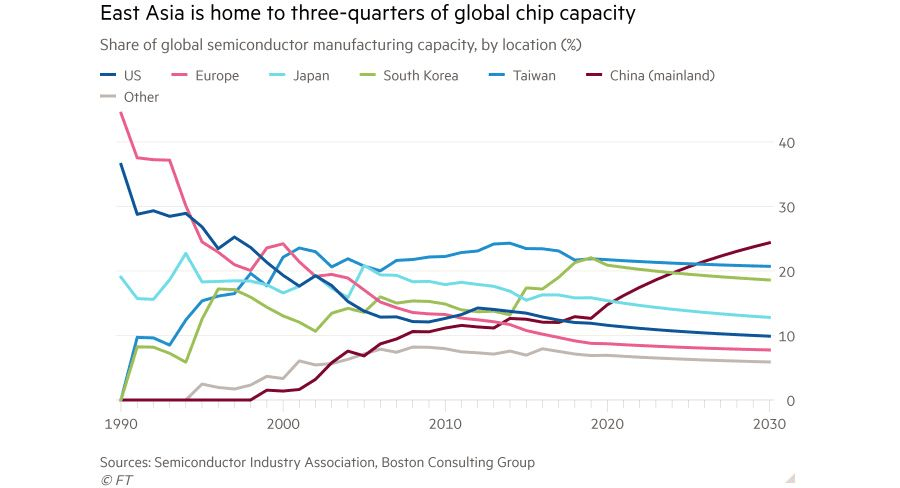

Asia is uniquely positioned to become the fulcrum of global semiconductor production, both in sheer scale and technological depth, as the world scrambles to meet soaring chip demand across industries. Not only does Asia command a formidable share of manufacturing, but policy initiatives, rising investments in advanced nodes, and consolidation of talent and supply chains are poised to secure its dominance well into the next decade.

Asia’s Semiconductor Boom: The Numbers

The growth trajectory is undeniable. The Asia-Pacific semiconductor device market is set to reach $504.99 billion by the end of 2025 and is projected to hit $753.76 billion by 2030, marking a compound annual growth rate of over 8%. Revenue projections for Asia’s semiconductor market in 2025 alone stand at $466.52 billion, constituting the largest regional share globally. Established manufacturing hubs—Taiwan, South Korea, and mainland China—continue to lead, but Southeast Asia, India, and Japan are swiftly closing the gap through purposeful policy shifts, foreign investments, and accelerating technology adoption.

Global Demand and Diversification

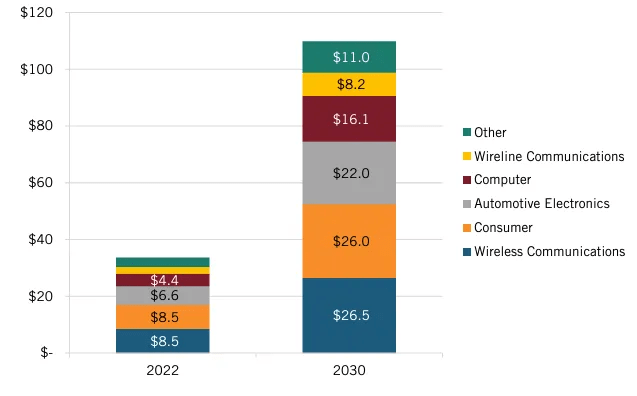

The relentless march of AI, IoT, 5G, electric vehicles, and edge computing is powering a structural surge in semiconductor demand. The automotive sector—especially with the electric vehicle (EV) revolution—has become a linchpin for new chip requirements, driving unprecedented volumes in China and a robust uptick in Southeast Asian countries like Indonesia, Malaysia, and Vietnam. GlobalFoundries’ $5 billion investment in Singapore for automotive chips is emblematic of how mature and advanced node demands are converging in Asia.

Moreover, the imperative to diversify supply chains amidst geopolitical volatility has propelled Southeast Asia and India to the forefront. The overreliance on Taiwan and China, exposed by disruptions and sanctions, has motivated multinationals to anchor in Malaysia, Vietnam, and India, which now offer cost efficiencies, competitive policy incentives, and an increasingly skilled workforce.

India and Southeast Asia: Rising Powerhouses

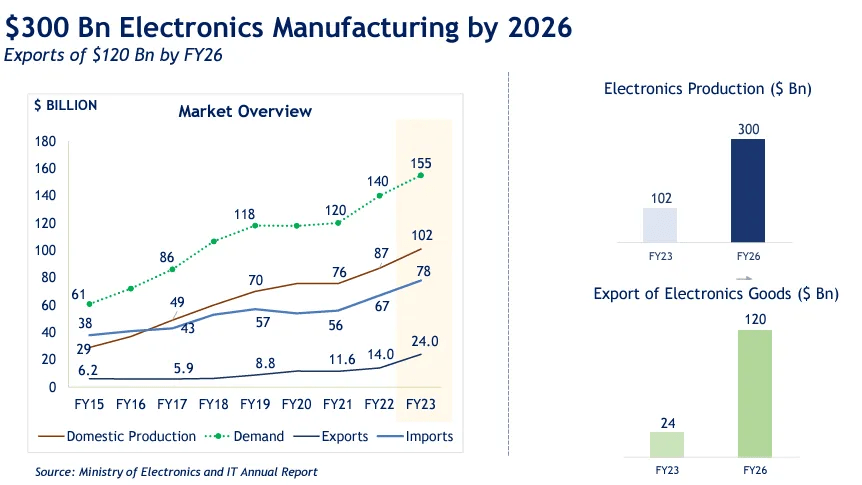

India’s semiconductor ambitions have transitioned from aspiration to action. With commercial chip manufacturing slated to begin by late 2025, buoyed by $18 billion in investments across 10 projects, India is strategically leveraging government incentives—such as the Production Linked Incentive (PLI) scheme and newly approved Electronics Component Manufacturing Scheme—to foster manufacturing self-sufficiency and global integration. These efforts have translated into a market growth forecast from $38 billion in 2023 to up to $50 billion by 2025, with an audacious target of $100–110 billion by 2030—if execution sustains pace.

Southeast Asia, on the other hand, is gaining recognition for its pivotal role in back-end operations—assembly, testing, and packaging (ATP)—vital processes that underpin the industry. Malaysia’s state of Penang has emerged as an AI chip assembly hotspot, clocking record investments and spurring government support for local GPU development. Vietnam and Thailand similarly bolster the region’s capacity and export orientation, making Southeast Asia a pillar of global chip supply resilience.

Strengths and Challenges in Asia’s Chip Landscape

Asia’s strengths extend beyond scale. The region houses dense, mature ecosystems—an interface of leading-edge fabs, supplier networks, research institutes, and global customers clustered for efficiency and innovation. Ongoing investments from industry leaders like TSMC, Samsung, Intel, and Infineon bolster both front-end advanced node manufacturing and back-end specialization. Meanwhile, tailored government incentives, R&D support, and preferential tax regimes catalyze competitiveness and continued upskilling of talent.

However, challenges persist. Skilled talent shortages, rising wage pressures, infrastructure gaps, and exposure to trade restrictions or tariff wars (as highlighted by Malaysia) may test the trajectory. Overcoming these bottlenecks demands disciplined investment in education, R&D, and supply chain security—Asia’s success will depend as much on execution as on grand announcements.

Asia’s chip hubs are advancing toward the technological frontier. As chip complexity grows from AI, IoT, and automotive needs, the region is scaling into advanced node manufacturing (down to 5nm and below), and rapidly adopting advanced packaging—such as FOPLP and CoWoS—required for high-performance applications. Taiwan’s TSMC, for instance, plans to double CoWoS capacity from 2024 to 2025, underlining how the region is becoming indispensable for leading-edge AI and data center chips.

Policy, Partnerships, and Regional Integration

Asia’s advantage is increasingly underpinned by proactive government policy and international partnerships. India’s Gujarat SemiConnect Conference and Japan’s $7 billion chip facility in partnership with TSMC and Sony are evidence of purposeful public-private collaboration spurring new value chains. The “China+1” strategy, where firms diversify manufacturing away from China while retaining its benefits, is being operationalized across Southeast Asia and India, both de-risking and enhancing global supply.

Simultaneously, Asia’s regional integration and open trade frameworks facilitate ecosystem synergies and rapid transfer of innovation, skills, and resources, fortifying the entire semiconductor value chain.

The Asian Century for Semiconductors

The world’s demand for semiconductors is growing insatiably, with the Asia-Pacific region now firmly at the heart of supply, innovation, and growth. As digital transformation deepens in every sector—from AI to EVs, from telecom to healthcare—Asian nations, led by both legacy and emerging players, have a generational opportunity to define the semiconductor industry’s future. Sustained investment, technical agility, and deft policy execution will determine whether Asia not only becomes the global chip hub but also retains the crown as the industry’s innovation engine for years to come.

References and Further Reading

- Deloitte. (2025, July 17). 2025 global semiconductor industry outlook. https://www.deloitte.com/us/en/insights/industry/technology/technology-media-telecom-outlooks/semiconductor-industry-outlook.html

- Infosys Knowledge Institute. (2025, April 6). Semiconductor industry outlook 2025. https://www.infosys.com/iki/research/semiconductor-industry-outlook2025.html

- Roland Berger. (2025, July 24). Southeast Asia in focus for semiconductor back-end. https://www.rolandberger.com/en/Insights/Publications/Southeast-Asia-in-focus-for-semiconductor-back-end.html

- Ken Research. (2025, July 30). Asia-Pacific Semiconductor Market Outlook to 2030. https://www.kenresearch.com/industry-reports/asia-pacific-semiconductor-market

- JLL. (2025, May 12). The booming semiconductor landscape in Asia Pacific. https://www.jll.com/en-in/insights/the-booming-semiconductor-landscape-in-asia-pacific

- IDC. (2024, December 11). Global Semiconductor Market to Grow by 15% in 2025. https://my.idc.com/getdoc.jsp?containerId=prAP52837624

- Statista. (2025, February 6). Semiconductors – Asia | Statista Market Forecast. https://www.statista.com/outlook/tmo/semiconductors/asia

- Source of Asia. (2025, March 12). Southeast Asia’s Semiconductor Role in Global Supply. https://www.sourceofasia.com/semiconductor-industry-in-southeast-asia-driving-global-innovation-and-supply-chains/

- Tech Wire Asia. (2025, September 2). Semiconductor India: Commercial chip production starts. https://techwireasia.com/2025/09/semiconductor-india-commercial-production-2025/

- ADB Blog. (n.d.). Asia’s Semiconductor Powerhouses Can Thrive in the AI Era. https://blogs.adb.org/blog/asia-s-semiconductor-powerhouses-can-thrive-ai-era

- Statista. (2025, January 27). Semiconductor industry in the Asia-Pacific region. https://www.statista.com/topics/11501/semiconductor-industry-in-the-asia-pacific-region/

- India Briefing. (2025, August 12). India’s Semiconductor Sector Outlook 2025. https://www.india-briefing.com/news/india-semiconductor-sector-outlook-2025-39067.html/

- ASEM Education. (2025, January 13). Why Malaysia is Emerging as a Global Semiconductor Hub. https://www.asemedu.com/2025/01/14/why-malaysia-is-emerging-as-a-global-semiconductor-hub/

- Allianz Trade. (2024, December 31). 2025 Semiconductor Report: Key Trends & Opportunities. https://www.allianz-trade.com/en_MY/insights/global-economic-insights/2025-semiconductor-report-key-trends-opportunities.html

- McKinsey & Company. (2025, April 20). Semiconductors have a big opportunity—but barriers to scale remain. https://www.mckinsey.com/industries/semiconductors/our-insights/semiconductors-have-a-big-opportunity-but-barriers-to-scale-remain

- Fortune Business Insights. (2024, October 31). ASEAN Semiconductor Market Size, Share & Forecast . https://www.fortunebusinessinsights.com/asean-semiconductor-market-105570

- EAC Consulting. (2025, January). Southeast Asia: Rising Pillar in Global Semiconductor. https://eac-consulting.de/wp-content/uploads/2025/01/EAC-Insight-SEA-Semicon.pdf